Our study of the production monohull and catamaran used boats markets in the 40-55 ft segment reveals a market undergoing profound transformation — and two worlds with radically different dynamics.

You will often hear that “the used sailing yacht market is suffering after the Covid bubble.” That is true, and it is false.

True, because the market no longer looks anything like what it once was.

False, because the usual narrative misreads both the mechanism and the segment that has actually been affected.

We have reviewed, on BoatWizard data *, every transaction and every listing of the last eight years across the five major monohull builders (Beneteau, Jeanneau, Bavaria, Hanse, Dufour) and the eight major catamaran builders (Lagoon, Fountaine Pajot, Catana, Bali, Leopard, Nautitech, Excess, Outremer) in the 40-55 ft range. The findings are more interesting — and more difficult — than the ambient narrative suggests.

*(the professional listing platform that feeds YachtWorld.com, Boats.com, Boat Trader, Annonces du Bateau, Cosas de Barcos, boot24, youboat, and others)

First surprise: monohulls did not experience a Covid bubble

It is generally assumed that used sailing yacht sales exploded during the Covid period before falling back. The numbers tell a different story.

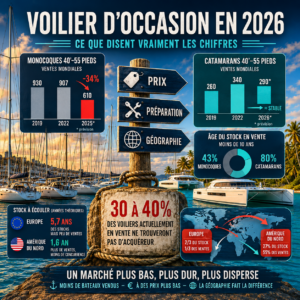

In 2022, at the supposed peak of the “bubble,” 907 monohulls in the 40-55 ft range from the five major builders sold worldwide. In 2019, the figure was 930. The same volume — neither more, nor less.

What Covid produced on monohulls were exceptional prices and exceptional demand — but not more transactions.

Buyers were many, but available inventory was limited. Today, the opposite holds true: boats for sale are overabundant, and buyers have largely disappeared.

On the monohull market, that is a 34% drop in sales between 2019 and 2025, and the 2026 trajectory extends the decline. More than a third of the market has vanished. And every brand is affected within a comparable range, between -31% and -45%. There is no protected niche.

Second surprise: the Covid bubble did happen — among catamarans

While monohulls remained stable in volume, the Lagoon, Fountaine Pajot, Bali and Leopard yards massively increased production. Demand was exploding (for charter, for families, for the comfort of space), delivery times stretched to three years, prices soared. A genuine production bubble, compounded by a charter bubble.

The trace of that bubble is still visible today — not in sales volumes, which remain remarkably stable (slightly above 2019), but in the abnormally young profile of the resale inventory: 80% of used 40-55 ft catamarans currently listed are less than 10 years old. On monohulls, that ratio is only 43%.

This demographic signature reflects two simultaneous phenomena: Covid-era buyers reselling earlier than expected, and charter fleet exits reaching their 5-year cycle. The catamaran market is not collapsing in volume, but its composition is changing profoundly — Bali has multiplied its sales by five, Outremer has tripled its own, Catana is in decline. The market is not dead — it has recomposed.

The hidden engine of catamaran production: an economic model that is breaking down

This explosion of catamaran production is not explained solely by the enthusiasm of recreational sailors for this type of boat.

For two decades, the catamaran industry has rested on a discreet but essential financial mechanism: charter management programs. In concrete terms, a charter company would sell a new catamaran to a private investor, who would entrust the boat to the fleet for 5 years, would collect a “return” presented as approaching 50% over the period, and would recover at exit a boat worth — typically — less than half its new-boat price.

In that scheme, the real buyer of a catamaran was often neither the sailor nor the charter company — it was the saver. The industrial margin on the boat sale largely covered the limited, sometimes negative, profitability of charter operations themselves.

The yards prospered by delivering at a sustained pace; the charter companies lived off the margins on boat sales more than off the rentals themselves.

That model is now breaking down. Rising new-boat prices, inflation in operating costs, the collapse of residual values, and the new generations’ lack of interest in this kind of “leisure investment” have caused the investor-buyer to largely disappear.

As long as pure charter operations are not profitable in their own right — which would require a major economic shift — the mechanism that fueled catamaran production for twenty years is broken. What we are seeing today on the used market is therefore not just the digestion of a Covid bubble: it is the beginning of a deep transition of the catamaran segment, of which we are likely seeing only the early stages.

The missing variable in the diagnosis: geography

This is perhaps the most telling finding of our study. Two thirds of worldwide monohull inventory sits in Europe. But only one third of transactions happen there.

Conversely, North America, which carries 27% of supply, accounts for 55% of sales.

In concrete terms: a monohull listed for sale in Europe faces 5.7 years of theoretical inventory to absorb before having an “average” chance of being sold. The same boat positioned in North America? 1.6 years. That is three-and-a-half times less competition.

The contrast is less extreme on catamarans (Europe 6.6 years vs North America 2.4 years), but the logic is the same: the European market is choked, the North American market remains relatively liquid. This imbalance transforms the fundamental sales question.

It is no longer just “what is my boat worth?”, it has become “where can my boat sell?”

Why the market is eroding — four underlying dynamics

None of these transformations is cyclical. They are cultural, demographic and regulatory, and they all converge in the same direction.

First, yacht ownership has lost its social value. Owning a sailing yacht no longer signals, no longer tells the same story it did twenty or thirty years ago. Where it once was a marker of achievement and adventure, it is now often perceived as a costly constraint, poorly aligned with contemporary lifestyles.

Second, younger generations rent rather than own. The boat is consumed as a service — a summer charter, a weekend, an experience — rather than as a legacy asset. This is a generational shift that touches every form of high-cost durable equipment.

Third, anchoring constraints are eroding the promise of freedom that long underpinned the imagination of cruising under sail. Restricted zones, quotas, paid mooring buoys, advance declarations: the ability to go where one wishes, to anchor where one wishes, is shrinking year after year. The prospective cruising-yacht buyer — who is buying first and foremost a project, a freedom, a horizon — sees that promise shrink.

Finally, tastes have evolved. Buyers are turning toward modern designs, wide hulls, panoramic saloons. And part of the demand that would have gone to a monohull ten years ago now chooses a catamaran. The monohull therefore suffers from a double penalty: a global decline in sailing demand and a partial migration of that demand toward multihulls.

A reality that must be named: a significant share of boats will not sell

At the end of this analysis, a finding imposes itself, and it is better said plainly than left to emerge between the lines.

In the market as it stands in 2026, we estimate that between 30 and 40% of the used sailing yachts currently listed for sale will not find a buyer. Not at their current price. Not within a reasonable timeframe. For some of them, not at all.

The arithmetic is unforgiving.

On the production monohull segment, 1,968 boats are listed for sale against roughly 420 transactions expected in 2026 — that is nearly five years of theoretical absorption if one assumes, implausibly, that no new boat would come on the market.

On the catamaran segment, 1,161 boats listed against approximately 290 annual sales.

And on the bluewater niche segments we have followed for twenty years, the ratios are equivalent, sometimes worse.

These numbers mean two things. First, that a significant share of currently listed boats is priced at levels the market will not validate. Second, that as time passes — carrying costs, erosion of value, deterioration of the listing — some of these boats will end up exiting the market by default: pulled from sale, kept reluctantly, or sold under conditions very far from the owner’s initial expectations.

This is not a comfortable message to deliver. But it is, in our view, the information that an honest broker owes their seller clients today.

What this means

The 2026 market is not a temporary dip that will eventually recover. It is a new normal, lower in volume, more geographically dispersed, harder to sell into. The 2022 price references reflected a bubble that no longer exists. The 2019 price references reflect a market that no longer exists either.

On the monohull side, this is a structural contraction, slow, lasting, with no prior bubble. On the catamaran side, this is the end of an industrial cycle sustained for twenty years by a charter-driven financing model that is no longer viable.

Two different stories that converge toward the same reality: fewer boats sold, at lower prices, on a market that geography makes even more demanding for European sellers.

For anyone wishing to sell today — be it a monohull, a catamaran, or a long-range cruiser — three levers have emerged as decisive: price, preparation, and geography. Waiting for the market to recover, or for the right buyer to travel, is no longer a strategy: in this context, it is the surest way not to sell.

The real question, in 2026, is no longer "what is my boat worth?". It has become: "is my boat among the 60 to 70% that will sell, or the 30 to 40% that will remain at the dock?". The answer to that question rests entirely on decisions that only the owner can make.